Blog

Guide

Why proof of funds checks are so important in conveyancing.

Introduction

If you’re buying a property, you may be asked to provide documents showing where your money is coming from. This can feel intrusive — especially when you’re already dealing with surveys, mortgage paperwork, and moving plans — but proof of funds checks are a normal and important part of conveyancing.

What are proof of funds checks?

Proof of funds checks are where your conveyancer confirms the following:

You have the money available to complete the purchase, and

The source of the money is clear (for example, savings, a gifted deposit, or proceeds from a sale)

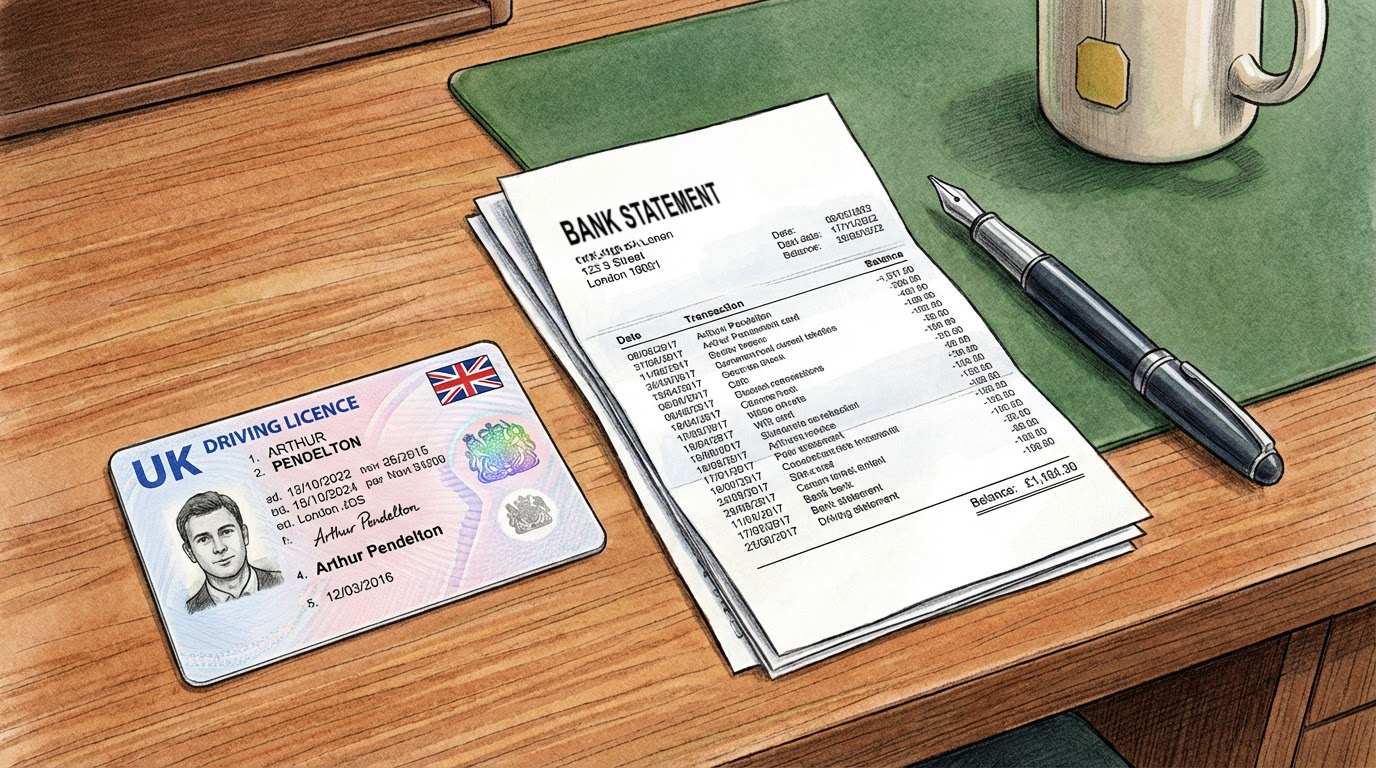

These checks usually involve seeing documents such as bank statements, savings statements, or evidence of a gift.

Why do conveyancers have to do this?

Conveyancers are required to carry out checks to help prevent money laundering and financial crime. Property transactions involve large sums of money, which is why the process includes identity checks and proof of funds requirements.

In simple terms, your conveyancer needs to understand where the purchase money comes from so they can act safely and lawfully.

What documents might you be asked to provide?

What’s needed can vary, but common requests include:

Recent bank statements showing savings building up over time

Savings account statements (ISAs, bonds, etc.)

Evidence of a gifted deposit, such as:

A signed gift letter.

The donor’s ID.

Statements showing the donor has the funds.

Sale proceeds evidence if your funds come from selling another property

Inheritance evidence (for example, a letter from a solicitor/executor)

Your conveyancer should tell you exactly what they need and why — and you can always ask if anything is unclear.

Tips to make it quicker and less stressful

Proof of funds checks are one of the easiest parts of the process to delay without meaning to. A few practical steps can help:

Gather documents early (even before searches and surveys are underway)

Avoid last-minute large cash deposits if possible, as these can require extra explanation

Keep a clear paper trail if money is being moved between accounts

Tell your conveyancer early if any deposit money is a gift, so the right steps can be taken from the start

A quick, clear response at this stage often helps prevent hold-ups later on.

Common concerns people have:

"Why do you need to see my statements?”

It’s not about judging your finances, it’s about meeting legal and regulatory requirements.

"Will this slow everything down?”

It doesn’t have to. When documents are provided promptly and clearly, checks are usually straightforward.

"What if my deposit is a gift from family?”

That’s common. It just needs to be documented properly so the transaction stays compliant.

Summary

Proof of funds checks can feel like an extra hurdle, but they’re a standard part of the conveyancing process and help protect everyone involved. Being prepared — and keeping your paperwork clear — can make this stage simple and stress-free.

At ArrowConveyancing, we understand how important it is to feel supported throughout the conveyancing process. Whether you're buying, selling, or just planning ahead, our experienced team is here to make things simpler, clearer, and more reassuring.

Visit: www.arrowconveyancing.co.uk

Call: 0116 266 5394

Email: hello@arrowconveyancing.co.uk

Disclaimer

The materials on this website do not constitute legal advice and are provided for general information only. Whether express or implied, no warranty is given concerning such materials. We shall not be liable for any technical, editorial, typographical, or other errors or omissions within the information provided on this website, nor shall we be responsible for the content of any web images or information linked to this website.

The information contained in this article does not constitute financial advice or recommendation and should not be considered as such. Arrow Conveyancing does not offer financial advice and is not regulated by the Financial Conduct Authority (FCA). The authors of this article are not financial advisors and aretherefore not authorised to offer financial advice.

Published on :

April 29, 2026

.png)